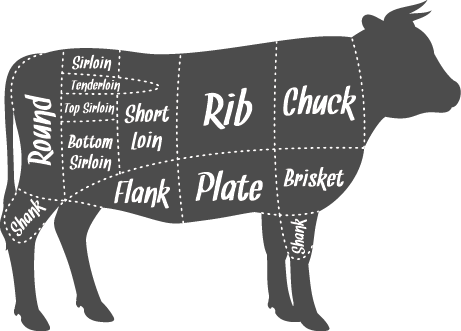

BEEF

The market is steady to firmer. Total beef production for last week was down 3.0% versus the prior week and down 2.8% compared to the same week last year. Year to date, total production is down 4.3% compared to the same period last year. Total headcount for last week was 593,000 as compared to 614,000 for the same week last year. Year to date, the total headcount is 4.76 million head which is down 5.4% from last year. Live weights for last week were down 1 lb. versus the prior week and up 7 lbs. from the same week last year. Beef cutout values are rising slightly as a result of limited supply, not increased demand. Packers increased supply to over 600K head per week for the last two weeks of January and demand was not enough to support those levels. More cutbacks are being reported and some plants may be reducing their production hours by 20% next week. Beef production is already behind 2023 levels and is dropping slightly on a weekly basis. Current slaughter levels are not harvesting the available amount of fed cattle as cattle-on-feed supplies are trending higher on the USDA’s cattle on feed report. On the demand side, grade-out is strong as prime and 2/3rds choice were reported to be up 1% in the first five weeks of the year. The choice cutout is posting record highs for the year. Cattle futures for March, April, and June are holding firm in anticipation of increased demand in the springtime months.

Grinds – The market is steady to firmer. Retail and QSR demand for the month of February has been moderate to good. Higher steer weights are helping keep the supply available. Availability varies among packers. Trade levels on 73% and 81% grinds are being pressured higher.

Loins – The market is steady. Demand from the retail and foodservice channels is average at best. The spread between choice and select remains tight. With supply constraining over the last couple of weeks, trade levels on choice and select are firm.

Rounds – The market is firmer. Demand patterns during February were reported to be good and mostly supported by the retail channel. As supply tightened during the month, availability got squeezed. Market levels are moving higher.

Chucks – The market is mixed. Overall demand is fair but varies on chuck and clods. Supply varies by packer depending on their weekly position. Trade levels are choppy and vary by supplier.

Ribs – The market is steady to firmer. Retail and foodservice volume is fair and tends to improve as we move into springtime. Availability and weekly trade levels vary depending on the packer. Reduced production has propped up trade values and market levels are inching higher.

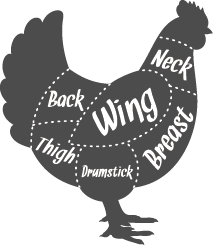

CHICKEN

The market is firmer. Total headcount for the week ending 2/24/2024 was 163,766,000 as compared to 167,098,000 for the same week last year. The average weight for last week was 6.43 lbs. as compared to 6.48 lbs. for the same week last year. Demand for chicken continues to impress as promotional activity on breast meat, tenders, and wings is highly robust. With red meat in short supply recently, more retailers and foodservice operators are using poultry as a key promotional driver. Future demand for boneless breast, tenders, and wings is expected to be strong with March Madness around the corner. Export demand for leg quarters and whole legs is showing weekly improvement and clearing supply adequately. Weekly supply is being challenged by lighter than expected bird weights. Market levels are showing strength across most poultry categories.

WOGS – The market is steady. Retail deli and fast-food demand was average at best in February. Demand for the premium sizes is reported to be good. Supply is available and varies by plant. Market levels are holding firm.

Tenders – The market is firmer. Foodservice and QSR volume are extremely robust and may continue through March. With vibrant foodservice demand, the portioning side of business gets an added bump in activity. Spot supply is tight. Market levels on jumbo and select sizes are moving higher.

Boneless Breast – The market is firmer. Volume from the retail, foodservice, and QSR channels continues to trend strong. Due to lack of red meat supply, grocers and QSR’s have been using boneless breast as a promotional lead. Supply remains tight for all sizes. The market for all sizes is being pressured higher.

Leg Quarters and Thighs – The market is firmer. Export and domestic demand for leg quarters is highly active and suppliers are trying to test the market at higher levels. Foodservice activity for thigh meat is very good. Supply varies by plant. The market on leg quarters is a full-steady and thigh meat is being pressured upward.

Wings – The market is firmer. March madness is right around the corner and foodservice demand is not showing any signs of slowing down. Further processing of small and medium wings is strong due to suppliers replenishing inventories. Supply is tight. The market is being pushed higher on all sizes.

SEA

Gulf Shrimp – The market is unsettled. Demand for domestic Gulf Shrimp has trended down due to competitive pressure from the import market.

Black Tiger Shrimp – The market is slightly weaker. The lower priced white shrimp market is helping to keep pressure on the Black Tiger market.

White Shrimp – The market is slightly weaker. A better balance between supply and demand is being reported, however, supplies remain adequate to fully adequate with moderate demand.

King Crab – The market is unsettled. Russian King Crab inventories continue to dwindle, due to the import ban imposed over a year ago. Demand for the remaining product is moderate to active.

Snow Crab – The market is steady to firmer. Demand has been moderate to active with supplies being adequate to barely adequate.

Warm Water Lobster Tails – The market is unchanged. The market has trended downward due to supplies being fully adequate and light demand. It is reported that volume sales are falling short of usual expectations.

North American Lobster Tails – The market is steady to firmer. Supplies are adequate to barely adequate with moderate demand.

Salmon – The market is weaker. Supply of Wild Salmon continues to rise and is not being met with similar demand. The market for frozen fillets out of Chile are barely steady. Supplies are adequate with moderate demand.

Cod – The market is steady to weaker. Demand remains below expectations as supplies continue to be adequate to fully adequate.

Flounder – The market is steady. The market is mostly unchanged.

Haddock – The market is steady to weaker. The market continues to be mostly unchanged while seeing lower pricing on all sizes. Supplies are reported as fully adequate with a quiet demand.

Pollock – The market is steady to weaker. Lack of demand has continued to put downward pricing pressure on the commodity.

Domestic Catfish – The market is steady to firmer. Demand for domestic catfish remains down due to competitive pressure from the import market.

Tilapia – The market is firmer. Reports of lighter supply and increased costs overseas are being met with moderate demand.

Swai – The market is weaker. Supplies are fully adequate, and demand remains lackluster.

Scallops – The market is steady to weaker. Recent landings have been on the lighter side, but demand has been barely adequate.

.

Cheese

The market is mixed. The CME Block market moved weaker as we progressed through the week and trended weaker than the week prior. The CME Barrel market moved firmer as we moved through the week and trended firmer than the week prior. Cheese processing continues to be limited by decreased milk volumes. According to the USDA, some cheesemakers say that lower milk availability has worked in their favor as running production schedules at capacity for most of the year was taxing on both the equipment and employees. Cheese production is overall reported as steady. Demand for cheddar is the strongest of the American-types cheeses. Mozzarella remains in high demand due to steady foodservice orders. Curd sales are reported as seasonally busy. Retail demand is reported as strong, while food-service demand is reported as steady across most regions.

In Europe, milk production is declining throughout many regions. Some cheesemakers have reported impacts to production due to tighter volumes while others are operating busy schedules to keep up with demand. Demand for cheese in Europe continues to outpace production. Retail demand for cheese is reported to be strong while food service demand is steady. Cheese prices are reported as steady to higher in Europe.

The market is firmer. The butter market trended firmer as the week progressed and moved firmer than the week prior. According to the USDA’s latest report, cream supplies are tight throughout the country. Demand for cream is far outpacing supply. Butter production overall is mixed. Some butter plant managers have noted that contracted loads of cream have helped to keep churns active while others report production schedules running less than anticipated volumes due to the lack of cream supply. Food-service demand for butter is reported as steady across most regions while retail demand is reported as softening. Export demand for butter is reported as moderate to light

The market is steady to weaker. In the retail sector, demand is being reported as fair. Foodservice and distributive business has declined as purchasers push off ordering to work through expensive holdover and bring in new inventories at cheaper prices. Export business continues to be good with supportive business coming from Canada, Mexico, and the Pacific Rim. Canada has maintained heavy demand in anticipation of their Thanksgiving.

Supply is available on medium and large sized shell eggs. Inventories have risen due to higher productivity and weaker demand. National weekly reports show shell egg inventory up 1.2% and breaking stock inventory up 7.4% over last week.

Demand in the egg products category remains moderate to good. Further processing business for raw whole egg and liquid whites is moderate and mostly transactional. Demand from Canada has been strong as they are in the middle of their Thanksgiving pull. With the increased export demand, a floor has been established, for the time being, in domestic values due to a lack of surplus. Discussions regarding holiday demand are currently quiet but may start picking up soon. Supply is available on liquid whites. Trade levels on liquid product and liquid whites are mostly flat, but strong undertones are starting to develop.

[tab title="Soy Oil"]

[tab title="Turkey"]

TURKEY

The market is steady. Total headcount for the week ending 2/24/2024 was 3,713,000 as compared to 3,551,000 for the same week last year. The average weight for last week was 31.86 lbs. as compared to 32.27 lbs. for the same week last year. Demand patterns for whole birds and turkey parts are static and mostly unchanged from the previous week. Booking season for whole birds began in early January and very little is being reported. Activity is fair on boneless breast while bone-in parts maintain stable demand. Export volume is fair, but HPAI restrictions are limiting overall activity. The supply side has a bit of uncertainty as industry participants wonder if and when the next HPAI outbreak may happen. While HPAI depopulated more birds in the 4th quarter of 2023 than the previous year, suppliers are carrying over more excess finished inventory into 2024. The supply side remains vigilant about bird health during these late winter months.

Whole Birds – The market is steady. The months of January and February were expected to be filled with booking activity, but the lack of firm commitments has the category spinning its wheels. The carryover of whole birds from 2023 into 2024 is being reported as higher than normal. Market levels are holding even.

Breast Meat – The market is steady to firmer. Further processor demand is on the rise for fresh tom breast meat. The supply of fresh is tight while supply on frozen is more available. The market is getting some upward pressure on the spot market.

Wings – The market is steady. Export volume for whole wings is fair at best and domestic demand for two-joints is outpacing supply. Supply is tight and varies on a plant-by-plant basis. The market on two-joints is being pressured higher on the spot market.

Drums and Thigh Meat – The market is steady to firmer. Export and domestic business on drums are status quo at the current time. Thigh meat demand is robust with good movement from the retail and further processing channels. Supply for thigh meat is short of industry needs. The market on drums is flat while thigh meat is getting some upward pressure.

SEAFOOD

Gulf Shrimp – The market is unsettled. Demand for domestic Gulf Shrimp is still unsettled due to competitive pressure from the import market. Comfortable trading levels remain to been seen.

Black Tiger Shrimp – The market is firmer. Tighter supplies of Black Tiger Shrimp and improved prices on White Shrimp have alleviated some of the downward price pressure on the Black Tiger Shrimp market.

White Shrimp – The market is firmer. Increased overseas pricing and improved movement have brought some stability back to the market. Supplies are adequate to barely adequate with moderate demand.

King Crab – The market is steady to slightly firmer. Supplies of King Crab, regardless of origin, are light with moderate to active demand. Inventories of Russian origin product continue to decline.

Snow Crab – The market is steady. Demand is moderate and supplies are adequate to barely adequate.

Warm Water Lobster Tails – The market is steady to barely steady. Despite the recent activity of North American Lobster Tails, there has been no impact on the Warm Water Lobster Tail market.

North American Lobster Tails – The market is firmer. Sellers continue to firm up prices to slow down demand and allocations remain in effect.

Salmon – The market is steady. The Chilean frozen fillet market is steady. Supplies are adequate with moderate demand. The European fillet market is steady. Supplies are adequate with fair demand.

Cod – The market is steady to weaker. Demand remains below expectations as supplies continue to be adequate to fully adequate.

Flounder – The market is steady and mostly unchanged.

Haddock – The market is steady to weaker. Supplies are reported as fully adequate with a quiet demand.

Pollock – The market is steady to weaker. Lack of demand has continued to put downward pricing pressure on the commodity.

Domestic Catfish – The market is steady to firmer. Demand for domestic catfish remains down due to competitive pressure from the import market.

Tilapia – The market is firmer. Light supply and increased costs overseas are being met with moderate demand.

Swai – The market is weaker. Supplies are fully adequate, and demand remains lackluster.

Scallops – The market is steady to weaker. Supplies are adequate with fair to weak demand.

. CHEESE

The market is weaker. Both the CME Block & Barrel market moved weaker as we progressed through the week. The Block market trended slightly weaker than the week prior. The Barrel market trended firmer than the weaker prior. Cheese production is overall steady. Some plant managers note that cheese inventories are comfortable despite slower production schedules. Demand for cheddar cheese is outpacing other American-type cheeses. Mozzarella continues to be the most in demand Italian-type cheese due to steady foodservice orders. Retail and food service demand is reported as steady across most regions. Export demand is reported as light.

In Europe, milk production continues to decline with some contacts indicating that volumes are at or below that of 2022 volumes. European cheesemakers are operating steady to lighter production schedules. According to the USDA, European cheese inventories are reported as tight. Demand for cheese in Europe continues to outpace production. Retail demand for cheese is reported to be strong while food service demand is steady. Cheese exports from Europe have been reported as unchanged.

[tab title="Butter"]

The market is weaker. The butter market trended weaker as the week progressed and the market moved weaker than the week prior. Cream supplies are reported as mixed depending on the region. Butter production is mixed overall. Contacts have relayed that production in the Central region is more comfortable for churning. Retail production is reported as strong to steady. According to the USDA’s latest report, several plant managers are working to build up their supply for the anticipated upcoming holiday demand. Domestic demand for butter has been reported as steady. Retail and food-service demand are reported as unchanged. Export demand for butter is reported as moderate to light.

The market is steady to firmer. Demand from the retail channel is getting an uptick in activity as retailers place orders for the Thanksgiving holiday. In addition, consumer baking tends to rise in November. Distributive business is showing improvement as buyers move up orders for holiday business. Based on historical trends, the month of November is when the category shows strength.

Supply is available on medium and large sized shell eggs. Market levels are moving higher on medium sizes and flat on large sizes. National weekly reports show shell egg inventory down 1.9% and breaking stock inventory down 2.5% over last week.

Demand in the egg products category is reported to be moderate. Demand for liquid whites, yolks, and dried items has been soft recently. These lower market levels may jump start the further processing side of the business. Trade levels on liquid product and liquid whites are mixed as suppliers and processors test the market.

FLOUR

The flour market is mixed. The wheat market was mixed as the week progressed due to soft export demand and competitive Russian pricing. The USDA’s February Crop Progress report shows sustained improvement for Hard Red Winter wheat crop conditions over last year and a mixed crop condition for Soft Red Winter wheat. According to the USDA’s most recent report, global production and trade are forecasted to be higher for the month of February though still anticipated to come in below last year’s numbers.

[/tab]

[tab title="Flour/Wheat"]

[/tab]

[/tabs]

[ tab title =